Buy The Peaceful Investor at Amazon

Table of Contents and Launch Site

I am offering the online chapters of the book using "The Honor System." Tip options at the bottom of the page.

Financial Literacy

Given the need for individuals to plan their own retirement, education is crucial. The Organisation for Economic Co-operation and Development (OECD) is an international group that researches global education. You may want to take a deep breath before reading these two definitions, but it’s worth the effort to have some perspective regarding how education impacts personal finance.

The OECD defines financial education asYou don't necessarily have to score high on a financial literacy test to be a successful investor. But being better educated should help. Socio-economic status and gender have modest correlation with financial literacy. But having a bank account and receiving monetary gifts favorably impacts financial literacy, while mathematics and reading scores have high correlations according data from “The Programme for International Student Assessment” (PISA). The organization assessed financial literacy in 13 OECD countries and economies by testing 29,000 15 year old students. U.S. students ranked right in the middle of the pack, above the Russian Federation, but below Latvia and Poland. Shanghai-China was the outlier with substantially better results than all the other countries and the Flemish community in Belgium came in second. The U.S. was the leader in only one category (for financial education being taught as a separate subject).11

“the process by which financial consumers/investors improve their understanding of financial products, concepts and risks and, through information, instruction and/or objective advice, develop the skills and confidence to become more aware of financial risks and opportunities, to make informed choices, to know where to go for help, and to take other effective actions to improve their financial well-being.”9The following definition of "financial literacy" was endorsed by the G20 (an international forum of large governments and central bank governors) leaders in 2012.

“Financial literacy is a combination of awareness, knowledge, skill, attitude and behaviour necessary to make sound financial decisions and ultimately achieve individual financial well-being”10

- Steven Kaplan and Joshua Rauh published a study in 2013 that analyzed the percentage of Forbes 400 members that were self-made versus those that inherited their wealth. The percentage of millionaires that were self-made rose from 40% in 1982 to 69% in 2011.12

- A 2013 BMO Capital Markets study concluded "two-thirds (67 percent) of high-net worth Americans are self-made millionaires, earning their wealth mostly on their own. Only three percent attributed their wealth to receiving an inheritance."13

- A 2016 U.S. Trust report summarized their survey of 684 high net worth and ultra-high net worth adults (with over $3 million in self-reported assets, not including the value of their primary residence).14 They found only 10% gained their wealth through inheritance, while 86% made their biggest gains with buy-and-hold strategies. The vast majority of respondents (77%) grew up middle class or poor, and their success was attributed to hard work, ambition, and family upbringing.

- In October of 2018 Forbes summarized that less than half the people on The Forbes 400 in 1984 "were self-made; in 2018, 67% of the 400 created their own fortunes."15

"Among emerging markets, East Asia is home to the large-scale entrepreneur. In contrast, the Middle East and North Africa is the only region where the share of inherited wealth is growing and the share of company founders is falling. Other emerging-market regions fall somewhere in between ... In Europe, inherited wealth still makes up the majority of billionaire wealth, while the growth in US billionaires has been driven by self-made wealth."

The Big Picture

Recent estimates place the number of people in the world at about 7.5 billion and the United States population at more than 320 million. The average life expectancy worldwide is about 71 years, while Americans are currently expected to live 78 years on average. Women live roughly five years longer than men on average. Japanese women have a life expectancy of 86 years, while Swiss men have an average life expectancy of 81 years, but those living in some less developed countries have much shorter life expectancies (some are in the 50s).

- At 1% interest that $300,000 grows to over $351,000

- At 2% that $300,000 grows to over $413,000

- At 3% that $300,000 grows to over $489,000

- At 4% that $300,000 grows to over $582,000

- At 5% that $300,000 more than doubles to over $695,000

- At 6% that $300,000 more than doubles to over $834,000

- At 7% that $300,000 more than triples to over $1,005,000

- At 1% that $360,000 grows to over $421,000

- At 2% that $360,000 grows to over $496,000

- At 3% that $360,000 grows to over $587,000

- At 4% that $360,000 grows to over $698,000

- At 5% that $360,000 more than doubles to over $834,000

- At 6% that $360,000 more than doubles to over $1,001,000

- At 7% that $360,000 more than triples to over $1,206,000

- A $1,000,000 portfolio implies $40,000 a year ($3,333 per month)

- $2,000,000 implies $80,000 a year

- $3,000,000 implies $120,000 a year

- $4,000,000 implies $160,000 a year

- $5,000,000 implies $200,000 a year

Social Security

The U.S. government created the Social Security program to provide some forced retirement saving and those that participate and contribute in their younger years (and meet the minimum requirements) receive social security benefits in their later years.25 But social security is not designed to be a primary source of retirement funding. It is best viewed as a supplement and hopefully provides one of several sources of income. There are legitimate concerns that social security in its current form cannot survive in the long run, but for now it is reasonably safe to assume that it will be a source for some cash flow for future retirees in the United States. Those in other countries may have similar programs that they can count on for income.

Yet, we have a relatively well-designed regulatory system governing the financial markets. The U.S. system based on capitalism allows competition to drive evolution of better products and services, which has resulted in a system with remarkable access and much lower costs than investors have experienced in the past. So let's quickly review some of the developments of the last century that have contributed to the evolution in investing based on the United States experience (many countries have similar structures and options).

1924 - The First Mutual Fund

Massachusetts Investors Trust was created on March 21, 1924, which initiated the mutual fund era. Mutual funds provide investors with the opportunity to diversify and choose managers to select securities rather than choose individual securities on their own (or by a broker or adviser). There are costs (primarily the mutual funds management fee) and potential tax implications, but the diversification via mutual funds is a major benefit for investors.1960 - Real Estate Investment Trusts (REIT)

REITs were created by congress in 1960 as a vehicle allowing investors to buy a portfolio of income producing real estate properties, similar to the structure mutual funds provide for investing in stocks. REITs can own many types of real estate including office or apartment buildings, rental homes, retail properties, warehouses, hospitals, shopping centers, hotels and even timberlands. Some REITs are also financial or mortgage based. The law was intended for income producing assets and REITs generally must pay out at least 90 percent of their taxable income in the form of dividends.1975 - Discount Brokers

In 1973 the Securities and Exchange Commission (SEC) announced that it would eliminate fixed commissions (which it did in 1975). It sounds "un-American" to me that investors weren’t able to negotiate commissions to buy securities (for over a century), but apparently that's the way it was. When the changes took effect, it opened the door for competition and discount brokers (like Charles Schwab, which was founded in 1971) soon began offering lower cost options for investors. That created the option for investors to open an account and buy a stock at more reasonable costs (without hiring a licensed full service broker or adviser). Whether an investor knows what he or she is doing, and how long they hold the security are separate questions of course. But at least the new options became available.1976 - Index Funds

John C. Bogle was known by most as “Jack Bogle” (he passed away in January 2019). He created the First Index Investment Trust at The Vanguard Group, the firm he founded. Some at the time described it as "Bogle's folly" and called it "un-American." Of course the investment industry has always been very lucrative and many rightfully felt their income was threatened by index funds. I'm not sure who would have predicted the vast amounts of money that would be invested in index funds, but there is no dispute that Bogle's creation of Vanguard and the first index fund has benefitted investors by remarkable proportions (more on Bogle and his legacy later).

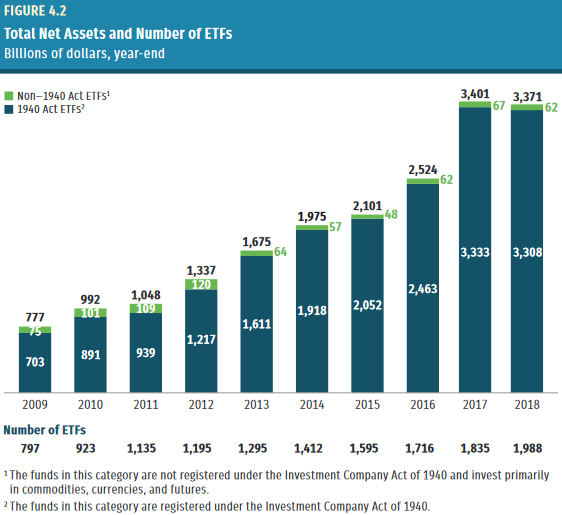

1993 - Exchange Traded Funds (ETF)

In 1993 the American Stock Exchange released the S&P 500 Depository Receipt (ticker symbol SPDR often called "spider"). This set off the Exchange Traded Fund (ETF) era. One advantage of ETFs is that they can be traded during the day by anyone with a brokerage account, unlike mutual funds which only trade on the close (plus all investors don't necessarily have equal access to all mutual funds depending on their brokerage accounts). As a result, you have more control over timing and pricing with ETFs. ETFs can also be actively managed, but the vast majority of ETF activity is in passive funds that track indexes. ETFs tend to have higher turnover, which implies many are using them for speculative purposes and there is some evidence that ETF investors tend to underperform mutual fund investors. ETF investors should also keep in mind the commissions and trading costs when transacting in ETFs, but when used appropriately they offer many advantages. The following chart from the Investment Company Institute shows the recent growth in the number and assets in ETFs.32

Source: ICI (page 83)1990s-2000s - Target Date Funds

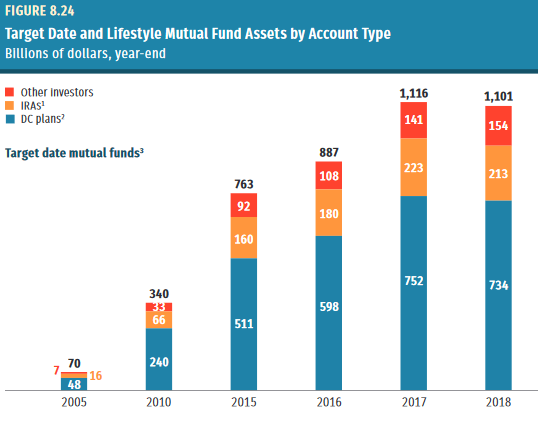

A more recent investing option is the creation of target date, or life cycle funds. The concept began taking shape in the 1990's and in the early 2000's target date funds began to accumulate substantial assets. According to Morningstar, Target-Date fund assets exceeded $1.7 Billion at the end of 2018.33 Target date funds are designed to provide a simple investment solution through a portfolio that becomes more conservative as time passes and the investor gets closer to the target (or retirement) date. Their popularity in the U.S. is fueled in part by efforts to improve retirement options through auto-enrollment and other techniques. They are designed to be attractive options for individuals as a simple, efficient, and appropriate investment option. They have become a type of default option for many employer linked retirement accounts. The following chart from the Investment Company Institute shows the recent growth in the number and assets in target date funds.34

Source: ICI (page 183)2010s - Robo-Advisors and Micro investing firms

As I mentioned in the preface, Financial Engines and other firms began offering automated services to investors in the 1990's, but more recently, so-called Robo-Advisor firms like Wealthfront, Betterment, and Acorns have been attracting substantial assets. Vanguard, Charles Schwab, Fidelity, Morningstar, and scores of others have also introduced variants, with many firms offering either pure technology based options, or hybrid offerings that combine technology and human interaction. I discuss the evolution of Robo-Advisors and how they are impacting the investment business in more detail in Chapter 30.

Overview

Ultimately this book is about the process of investing, but it is also about sleeping well and being comfortable and confident in your investing. So the first step is actually getting your head in the right frame of mind. Chapter two begins with some perspective on how money and wealth fit into the big picture. Before discussing finance and investing, in chapter three I discuss psychology, behavioral finance and how people think about money and risk. Next comes an introduction to the business of investing, which leads into a discussion of what financial activities are actually investing (which investors should focus on) versus those that are speculative (which investors should most likely avoid). I then move onto how financial markets operate in discussing the efficient market hypothesis and the random walk theories.

Table of Contents and Launch Site

Notes - The Footnotes in the Book are sequential and for this chapter start at #3 and end at #46.

1. United States Government Accountability Office (May 2015) citing Department of Labor http://www.gao.gov/assets/680/670153.pdf

2. http://science.sciencemag.org/content/339/6124/1152

http://faculty.chicagobooth.edu/richard.thaler/research/pdf/Behavioral%20Economics%20and%20the%20Retirement%20Savings%20Crisis.pdf

3. https://www.gobankingrates.com/investing/why-americans-will-retire-broke/

4.Charles Ellis, “Our #1 Challenge: Retirement Insecurity" Financial Analysts Journal, Fourth Quarter 2018

https://www.cfapubs.org/doi/pdf/10.2469/faj.v74.n4.2

Ellis suggests "Best Practices" including automatic participation in defined contribution plans (unless opting out), the use of target date funds, and low cost index funds.

5. http://www.bankrate.com/finance/consumer-index/financial-security-charts-0217.aspx

6. http://www.bankrate.com/pdfs/pr/20160706-July-Money-Pulse.pdf

http://www.bankrate.com/finance/consumer-index/money-pulse-0716.aspx

7. https://www.cnbc.com/2018/03/06/42-percent-of-americans-are-at-risk-of-retiring-broke.html

8. http://www.usfinancialcapability.org/downloads/NFCS_2015_Report_Natl_Findings.pdf

9.(OECD, 2005) https://www.oecd.org

10. Adele Atkinson, Flore-Anne Messy 2012 Measuring Financial Literacy

http://www.oecd-ilibrary.org/finance-and-investment/measuring-financial-literacy_5k9csfs90fr4-en

11. PISA 2012 Results: Students and Money Financial Literacy Skills for the 21st CENTURY

https://www.oecd.org/pisa/keyfindings/PISA-2012-results-volume-vi.pdf

12. Steven Kaplan, Joshua Rauh, "Family, Education, and Sources of Wealth among the Richest Americans, 1982-2012," American Economic Review, May 2013 https://www.aeaweb.org/articles?id=10.1257/aer.103.3.158

13. https://newsroom.bmo.com/2013-06-13-BMO-Private-Bank-Changing-Face-of-Wealth-Study-Two-Thirds-of-Nations-Wealthy-Are-Self-Made-Millionaires

14. https://newsroom.bankofamerica.com/press-releases/global-wealth-and-investment-management/us-trust-study-finds-10-common-success

15. https://www.forbes.com/sites/luisakroll/2018/10/03/the-forbes-400-self-made-score-from-silver-spooners-to-bootstrappers/#2330e01b6cd9

16. https://en.wikipedia.org/wiki/Millionaire - Some estimate many more, for instance https://dqydj.com/how-many-millionaires-decamillionaires-america/

17. Peterson Institute for International Economics, "The Origins of the Superrich: The Billionaire Characteristics Database" February 2016 https://piie.com/publications/wp/wp16-1.pdf

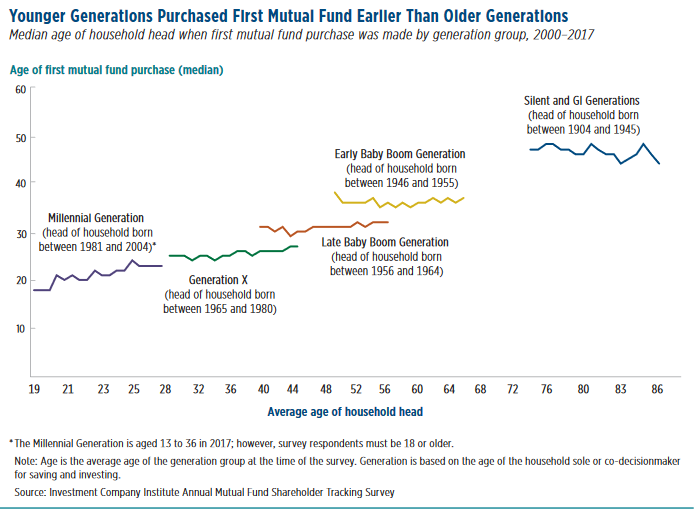

18. See page 19 of https://www.ici.org/pdf/per23-08.pdf (Characteristics of Mutual Fund Investors, 2017) for a visualization of age of first mutual fund investment purchase by generation.

19. https://www.ici.org/pdf/per23-08.pdf Characteristics of Mutual Fund Investors (see graphic on page 19 for investing ages)

20. https://www.quora.com/How-many-people-are-born-die-every-day-in-the-world-What-is-birth-to-death-ratio-in-the-world

21. The U.S. government's IRA Required Minimum Distribution Worksheet is a good tool for estimating cash flow withdrawal rates because it sets the minimum you must withdraw from your tax deferred accounts, based on your age. At age 70.5 you must start withdrawing your balance divided by the distribution period. At that age it is 27.4, which equates to about 3.65%. By Age 73 the distribution period is 24.7 which equites to more than 4%.

22. https://www.irs.gov/pub/irs-tege/uniform_rmd_wksht.pdf">

23. https://www.morningstar.com/articles/917708/your-rmd-amounts-are-more-conservative-than-you-mi.html

24. https://www.aboutschwab.com/schwab-401k-participant-study-2019

25. https://www.ssa.gov/myaccount/

26. https://www.ssa.gov/news/press/factsheets/basicfact-alt.pdf (accessed 12/6/2018 - 2019 was 64 million as of 4/11/2019)

27. US Census Bureau, Income Distribution to $250,000 or More for Households: 2013". Census.gov. Retrieved 2015-03-02

28. https://fred.stlouisfed.org/series/MAFAINUSA646N

29. http://news.gallup.com/poll/225023/investors-no-strings-attached-retirement-income-stream.aspx

30. Laurence Siegel "After 70 Years of Fruitful Research, Why is there Still a Retirement Crisis" January/February 2015 Financial Analysts Journal https://www.cfapubs.org/doi/full/10.2469/faj.v71.n1.1

31. https://www.ici.org/pdf/2019_factbook.pdf (page 74) or https://www.icifactbook.org/ch3/19_fb_ch3

32. https://www.ici.org/pdf/2019_factbook.pdf (page 83) or https://www.icifactbook.org/ch4/19_fb_ch4

33. Price Continues to Rule the Target-Date Fund Landscape, May 20,2019 https://www.morningstar.com/articles/929906/price-continues-to-rule-the-targetdate-fund-landsc.html

34. http://www.icifactbook.org/deployedfiles/FactBook/Site%20Properties/pdf/2018/2018_factbook.pdf (page 197)

The 2019 version shows a slight decrease in assets in 2018 https://www.ici.org/pdf/2019_factbook.pdf (page 183) or https://www.icifactbook.org/ch8/19_fb_ch8

35. http://www.schroders.com/en/sysglobalassets/digital/insights/2017/pdf/global-investor-study-2017/theme2/schroders_report-2__eng_master.pdf

36. Sendhil Mullainathan, Markus Noeth, Antoinette Schoar, Conflicts who can you Trust The Market for Financial Advice: An Audit Study NBER Working Paper No. 17929 Issued in March 2012 http://www.nber.org/papers/w17929, https://www.kitces.com/blog/how-the-advisor-sting-study-completely-missed-the-mark/

37. Joseph C. Peiffer and Christine Lazaro BROKERAGE INDUSTRY ADVERTISING CREATES THE ILLUSION OF A FIDUCIARY DUTY Misleading Ads Fuel Confusion, Underscore Need for Fiduciary Standard (3/25/2015) https://piaba.org/system/files/pdfs/PIABA%20Conflicted%20Advice%20Report.pdf

38. https://www.wsj.com/articles/advisers-at-leading-discount-brokers-win-bonuses-to-push-higher-priced-products-1515604130 (1/11/2018 print edition)

39. https://www.barrons.com/articles/the-great-fund-fee-divide-1515214360 (1/6/2018)

40. https://www.federalreserve.gov/releases/z1/20180308/z1.pdf 4Q2017 Z.1 data on households http://jlfmi.tumblr.com/post/171919215760/household-stock-exposure-inches-closer-to-dotcom

41. https://news.gallup.com/poll/233699/young-americans-wary-investing-stocks.aspx (5/4/2018) http://news.gallup.com/poll/211052/stock-ownership-down-among-older-higher-income.aspx (5/24/2017) http://news.gallup.com/poll/190883/half-americans-own-stocks-matching-record-low.aspx (4/20/2016)

42. https://www.bankrate.com/investing/did-you-miss-the-stock-market-rally-youre-not-alone/ (4/9/2015)

43. https://qz.com/1272280/there-are-now-almost-as-many-equity-funds-as-there-are-stocks-for-them-to-invest-in/

44. https://www.institutionalinvestor.com/article/b1dd82391ds6sz/Allocators-Need-Them-Asset-Managers-Resent-Them-And-Everyone-Is-Afraid-of-Them

If you don't think the material was worthwhile, I would appreciate emails letting me know what you read and whether you disagree with anything in particular. I would also appreciate anyone letting me know if they find any typos, mistakes, or suggestions how to improve the material.

- Paypal me at gkarz@aol.com

- Pay me by credit card. Email me (proficient at aol.com) with an amount you'd like to donate and I will email you an invoice via Square.com. I will not have access to your information - you would enter it on the secure square website.

- Before you make purchases at Amazon, link through one of my links. As an Amazon Associate I earn from qualifying purchases.

- Contact me to inquire about a review or second opinion of your finances.

Gary Karz, CFA

Author of The Peaceful Investor and Publisher of InvestorHome.com

twitter.com/GKarz (email)