The earliest investment portfolio and asset allocation recommendation dates back more than a millennium and it's relevance to modern investing was rediscovered by prominent investment professionals in the United States more than three centuries ago. The first time I recall reading about a "Talmud" strategy was in Jack Bogle's book Common Sense on Mutual funds, but many others have cited what is often referred to as “The Talmud Portfolio.”

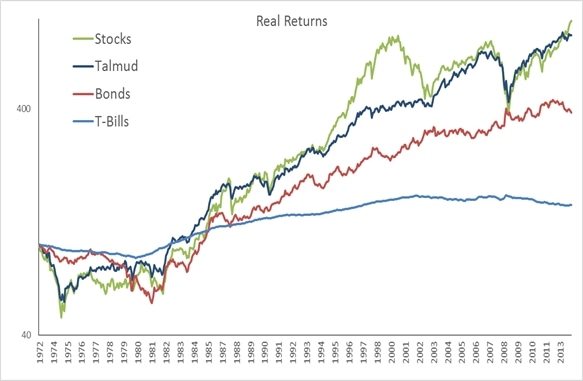

Category Equity (business) Real Estate Bonds US only Talmud Portfolio 1/3 VTI 1/3 VNQ 1/3 BND Global Talmud Portfolio 1/3 VT (or other) 1/3 REET (or VNQ/VNQI) 1/3 BND/BNDX (or AGG/IAGG) Global Capital Stock (2015) 33% Private & Public Equity 22% Global Real Estate & Land World Market Wealth (1980) 33% Foreign + 20% US Real Estate

The Talmud Portfolio from Salvador Litvak on Vimeo.

Gary Karz, CFA

Author of The Peaceful Investor and Publisher of InvestorHome.com

twitter.com/GKarz (email)

Check out Peaceful Investor at Amazon